Every few years, a company goes public with so much fanfare that it feels like missing the opening bell means missing the boat entirely. We've seen it with Facebook, Uber, Snap, and Lyft — and now the buzz is building around the likes of OpenAI and SpaceX. The hype is electric. The CNBC chyrons are breathless. And retail investors, afraid to be left behind, pile in on day one.

Here's what history consistently shows: that's usually the worst time to buy.

High-profile IPOs often surge at the open, cool sharply, and spend years clawing back to their offering price — and that pattern is not just a feeling, it's well-documented. Historical data indicates that many IPOs lag the broader market for up to two and a half years as early enthusiasm fades and insider selling increases the supply of shares. The technology sector, where almost all the buzz IPOs come from, has historically been the most dramatic corner of the IPO market.

Let's look at the evidence — and a few exceptions worth noting.

Before diving into the case studies, it helps to understand why this pattern repeats so reliably. There are three forces at work.

First, pricing. Investment banks price IPOs to generate excitement, not to maximize the share price. A stock that pops 20% on day one looks like a success — the company raised its capital, and early institutional investors made a quick return. But that pop is essentially money left on the table that retail buyers happily hand over.

Second, the quiet period. In the 25 days following an IPO, underwriters are restricted from publishing research. Once that period ends, analyst coverage begins — and the reports are almost always rosy (the banks vetted these companies before taking them public, after all). This coverage can push prices in either direction, introducing another wave of volatility.

Third — and most importantly — the lockup expiration. When a company goes public, insiders (founders, early employees, venture capital firms) are prohibited from selling their shares for a legally specified period, typically 90 to 180 days. When that lock lifts, a flood of supply hits the market. Research from the University of Florida's Professor Jay Ritter shows that IPOs underperformed comparable companies by 0.3% in their first six months — but that underperformance widened to 5.6% in the following six months, right as lockups were expiring. The pattern is consistent enough that many experienced investors treat the lockup expiration as a natural buying window.

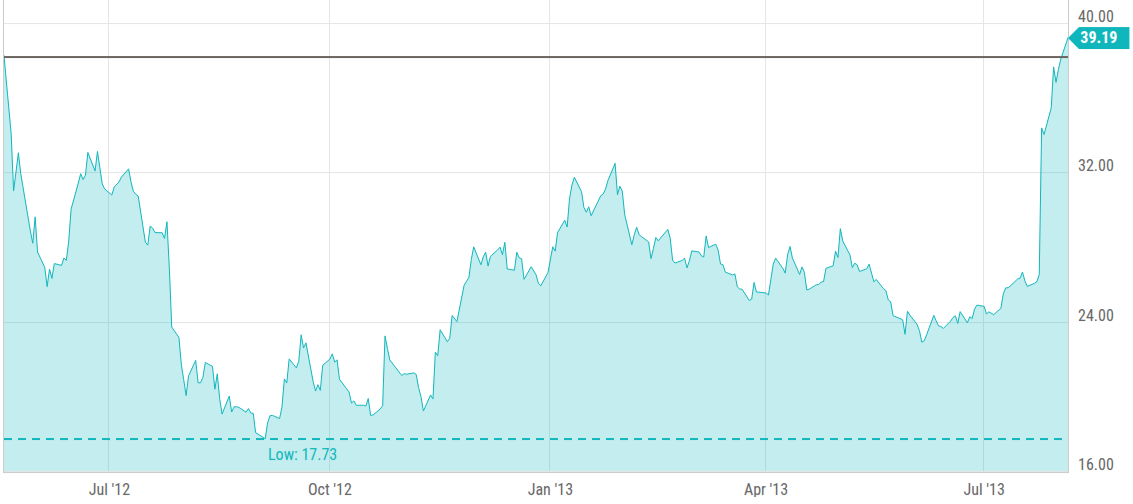

IPO price: $38 | Low: ~$17.73 | Time to recover: ~14 months

No IPO better illustrates the trap than Facebook's May 2012 debut. It was the most anticipated tech offering in years — and it stumbled almost immediately. NASDAQ's own order-handling system glitched on the opening day. Morgan Stanley reportedly had to actively buy shares just to keep the price from falling below $38 on day one. Within three months, the stock had fallen roughly 50%, bottoming out near $18 in September 2012 as the first lockup expiration arrived, allowing early venture investors like Accel Partners and Meritech Capital to cash out.

It took more than 14 months for Facebook shares to recover to their $38 IPO price. But investors who bought at the bottom — around $18 — and waited for the mobile ad business to prove itself were rewarded handsomely. A $5,000 investment at the IPO price grew to roughly $25,000 by 2019. The same $5,000 invested at the September 2012 low would have grown to nearly $34,000. Patience, in this case, was worth about $9,000.

IPO price: $17 | First-day close: ~$24 | Result: Still below IPO price years later

Snap's March 2017 debut is a textbook example of the first-day pop that never leads anywhere good. Shares surged 44% on opening day, closing around $24. Within two years, the company's stock had been cut in half, trading below $11 — well beneath even the original offering price. Investors who bought at the euphoric first-day peak suffered losses that, for many, never recovered. Snap remains a warning that even patient waiting doesn't guarantee a return if the underlying business fails to deliver.

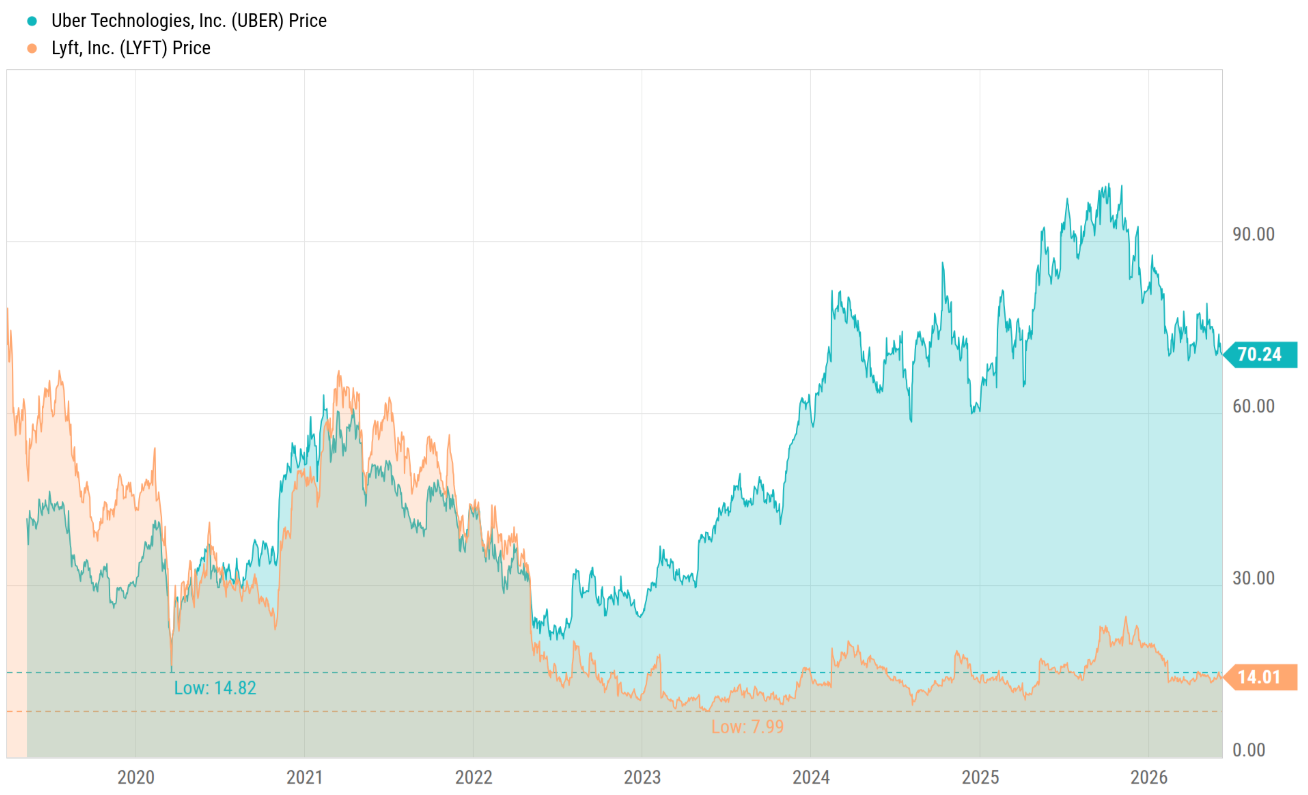

Uber IPO price: $45 | Low: ~$26 | Lyft IPO price: $72 | Low: ~$14.50

The 2019 ride-share IPO wave was supposed to be a defining moment for tech investing. Instead, it became a lesson in hype versus fundamentals. Lyft priced its IPO at $72 — above its initial range — and opened above $87. By its second trading day, it had already fallen below the offering price. Within months, both Uber and Lyft had hit record lows. By October 2019, Uber was down nearly 40% from its all-time high, and Lyft had fallen 56% from its peak.

The pattern held: institutional investors and insiders — who had driven up private valuations for years before the IPOs — had already captured the bulk of the gains. Public market buyers inherited the risk.

Uber's story does have a silver lining. The stock has since recovered and trades significantly above its IPO price, making it one of the better long-term outcomes from that class. But investors who waited 12 to 18 months after the IPO entered at far better prices than those who rushed in on day one.

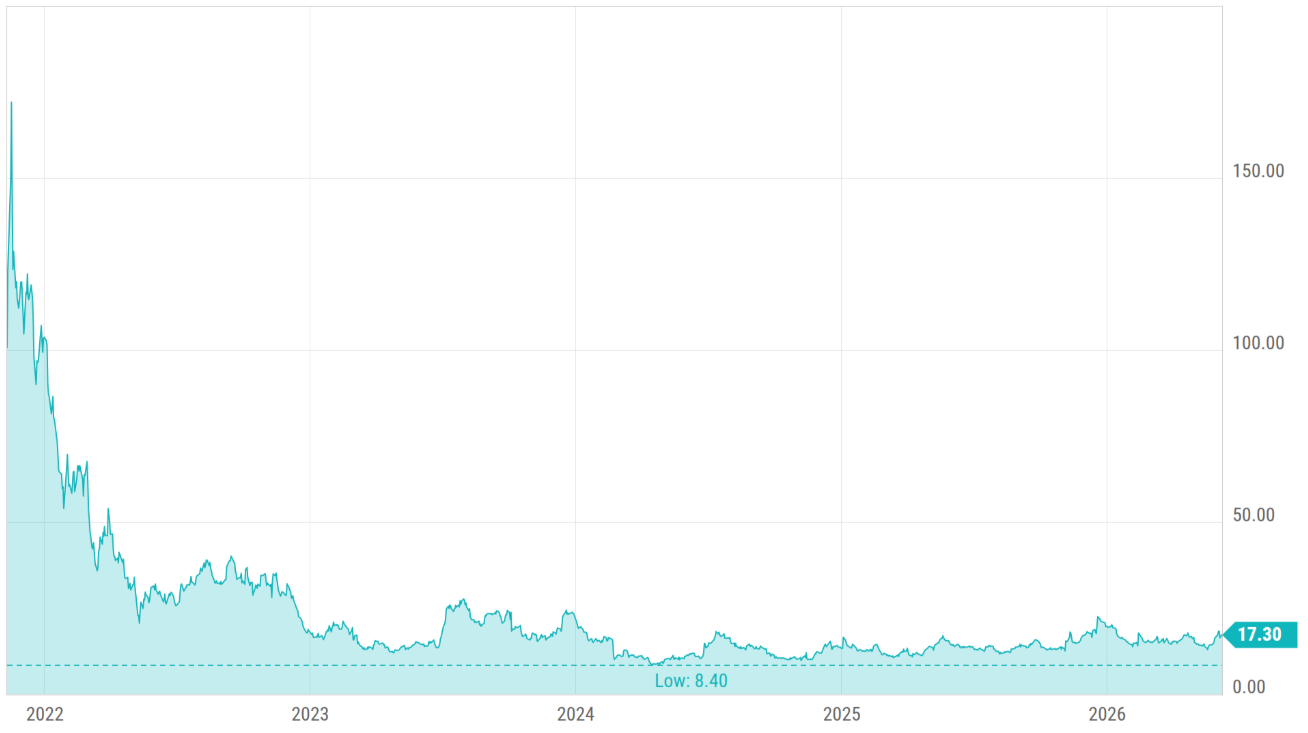

IPO price: $78 | Subsequent decline: ~85% below offering

Rivian's 2021 debut was the largest EV IPO in history, raising $11.9 billion. It arrived at the peak of the EV euphoria cycle. The stock briefly exceeded $170 per share in the weeks following the IPO before the broader EV revaluation took hold. Today, Rivian trades roughly 85% below its offering price. Investors who rushed in at the top are still waiting for a recovery that may never come at that price level.

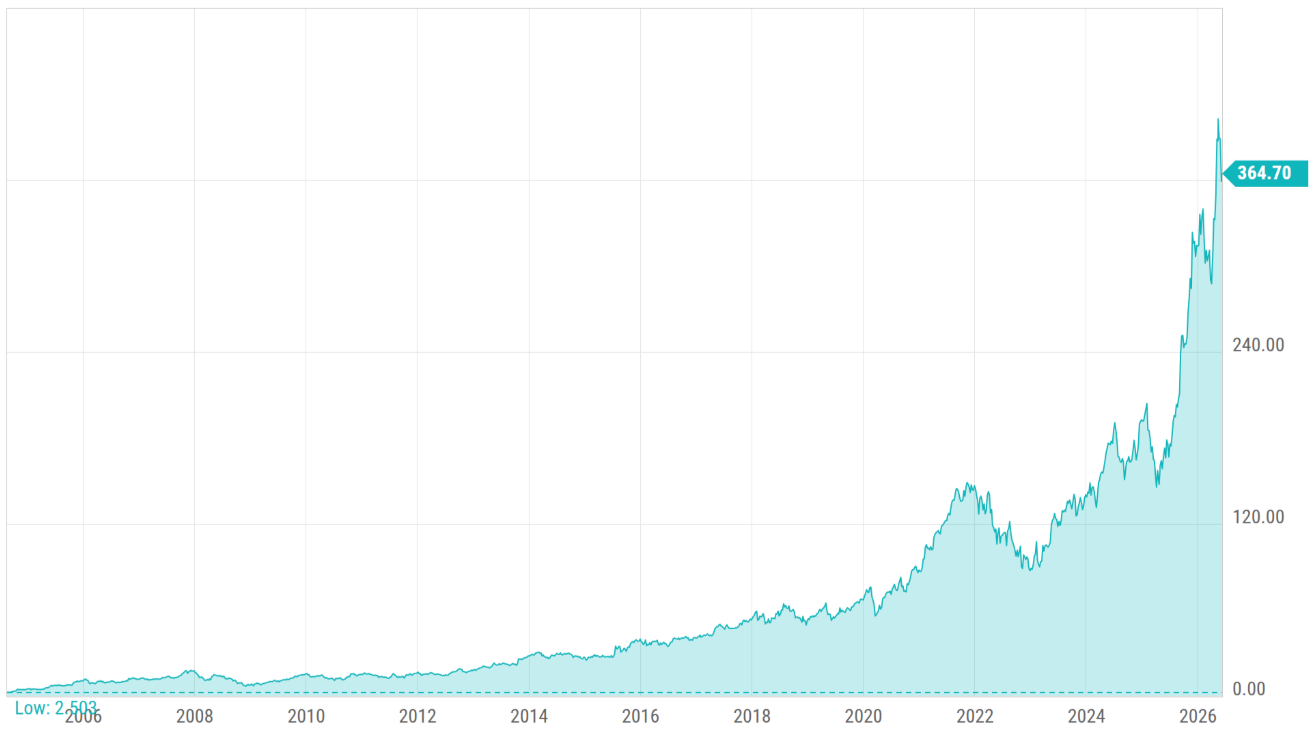

Every rule needs its exception, and Google's August 2004 IPO is the clearest one on record.

Google came public at $85 per share — already a reduced price from its original target range of $108 to $135, after a rocky road through its unusual Dutch auction format and the lingering hangover of the dot-com crash. On its first day, the stock jumped 18% to just over $100. And it essentially never looked back.

Unlike the companies above, Google was already dominant (handling more than half of all global web searches by 2003), already revenue-positive ($3.2 billion in annual sales), and already diversified into adjacent businesses. Investors who bought on day one at $85 and held have averaged a 24.8% annual return over the following two decades — one of the best long-term track records of any major IPO in history.

Google is the exception that proves the rule: when a company is already a proven cash machine with dominant market position, the IPO price can genuinely be the best entry point. The question for every hyped IPO is whether the company in front of you is actually Google — or just wants you to think it is.

Based on historical patterns, there are three windows worth watching:

Window 1: The Quiet Period End (~25 days post-IPO) When analyst coverage launches, it often moves the stock. The reports are typically positive, which can provide a small lift — but more importantly, increased transparency sometimes brings the price down as reality tempers hype. This is a minor window, but worth monitoring.

Window 2: The Lockup Expiration (90–180 days post-IPO) This is the most reliable structural entry point for patient investors. When insiders are finally allowed to sell — and many do — the increased supply puts downward pressure on price. The drop is often 5–15%, sometimes more. If you believe in the company's long-term fundamentals, the lockup expiration window is historically one of the better times to establish or add to a position.

Window 3: 6–12 Months Post-IPO Market data shows that some of the strongest IPO investments are made six to twelve months after listing. By this point, expectations have been reset, insider selling has largely run its course, and institutional ownership has stabilized. You also have multiple earnings reports to evaluate, which removes significant uncertainty.

The general principle: let the stock find its floor before you buy. For most high-profile IPOs, that floor arrives well after the opening bell.

The history is clear — and the data backs it up. Most high-profile IPOs, particularly in the technology sector, follow a predictable arc: initial pop, extended decline, slow recovery. The investors who do best are rarely the ones celebrating in front of CNBC on IPO day. They're the ones who waited, watched, and bought when everyone else had moved on.

The exceptions — companies like Google, Visa, or Amazon — exist. But they share a common trait: they were already proven businesses at the time of their IPOs, not just compelling stories. As OpenAI, SpaceX, and others approach the public markets, that's the question worth asking before you reach for the buy button on day one.

This article is for informational and educational purposes only and should not be construed as financial advice. Past performance of IPOs is not indicative of future results. Always consult a qualified financial advisor before making investment decisions.